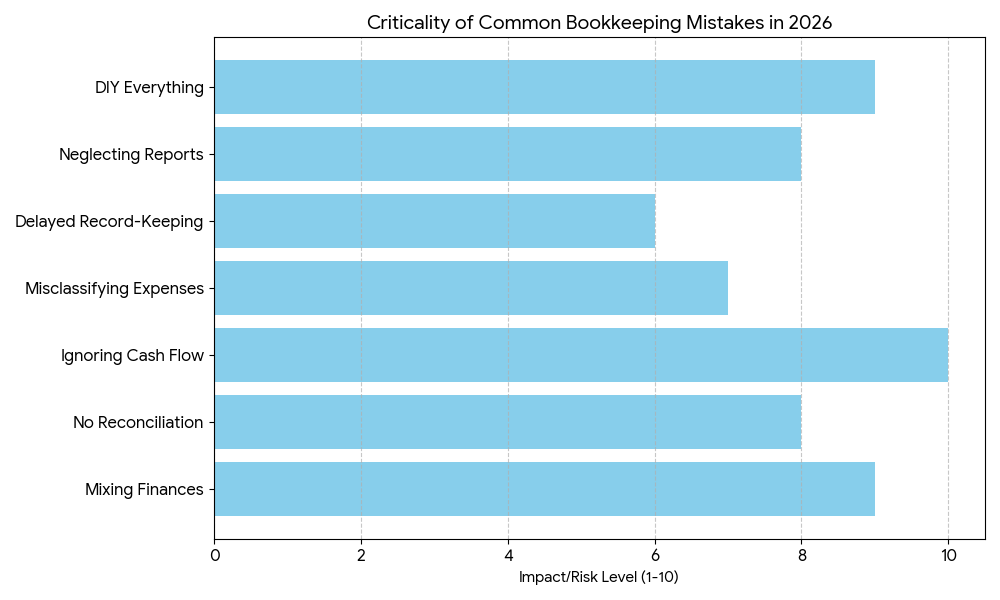

Avoid Financial Loss: 7 Critical Bookkeeping Mistakes Small Businesses Make in 2026

For many small business owners, bookkeeping is often viewed as a “necessary evil”—a tedious administrative task pushed to the bottom of a busy to-do list. However, in 2026, where digital integration and economic shifts are moving faster than ever, neglecting your books is no longer just a chore; it is a direct path to preventable financial loss.

When your financial records are inaccurate, you are flying blind. You may miss tax deductions, suffer from cash flow crises, or even face legal and compliance penalties. Below are the 7 most critical bookkeeping mistakes that small businesses must avoid to remain profitable and sustainable this year.

1. Mixing Personal and Business Finances

This is the “original sin” of small business accounting. Using your personal checking account for business expenses (or vice versa) creates a nightmare for your records.

-

The Risk: Beyond the headache of trying to untangle transactions at tax time, you risk “piercing the corporate veil.” If you operate as an LLC or corporation, mixing funds can legally jeopardize your limited liability protection, potentially leaving your personal assets vulnerable in the event of a lawsuit.

-

The Fix: Open a dedicated business bank account immediately. Use a business-specific credit card for all company purchases. Treat your business as a separate entity—if you need to take money out, perform a formal owner’s draw or salary transfer.

2. Failing to Reconcile Accounts Regularly

Bank reconciliation is the process of matching your internal records against your bank statements. Many owners skip this, assuming their accounting software is “always right.”

-

The Risk: Software can only process what is fed into it. Missed entries, bank errors, fraudulent charges, or duplicate transactions often hide in the gap between your books and the actual bank balance.

-

The Fix: Make bank reconciliation a non-negotiable monthly ritual. By verifying every transaction once a month, you catch errors while they are still fresh and easy to fix, rather than trying to audit a year’s worth of transactions at tax season.

3. Ignoring Cash Flow Management

Profitability is not the same as cash flow. You can be “profitable” on paper because you’ve made a sale, but if the client hasn’t paid, you have no cash to pay your own staff or vendors.

-

The Risk: Misunderstanding this difference leads to “paper profits” that leave you unable to cover payroll or operational costs, forcing businesses into high-interest debt or bankruptcy.

-

The Fix: Use your bookkeeping software to generate a Cash Flow Statement regularly. Monitor your Accounts Receivable (money owed to you) and set up automated reminders for overdue invoices to ensure revenue actually hits your account.

4. Misclassifying Expenses

Are your office supplies actually “equipment”? Did you label a lunch as a “travel expense” instead of “meals”? Tax authorities are strict about categorization.

-

The Risk: Misclassification can lead to audit flags. Furthermore, you may be overpaying your taxes by failing to claim the correct deductions or underpaying by claiming things you shouldn’t—both of which result in costly penalties and interest.

-

The Fix: Maintain a clear, standard Chart of Accounts. If you aren’t sure how to classify a specific expense, consult with an accountant once to set up a template, and then stick to it consistently throughout the year.

5. Falling Behind on Record-Keeping

In 2026, the “receipt in a shoebox” method is effectively a death sentence for your business’s financial accuracy.

-

The Risk: When you wait too long to record transactions, human memory fails. You will forget what that $50 charge on your statement was for. You also lose the ability to make real-time decisions based on your actual financial position.

-

The Fix: Embrace cloud-based accounting and mobile receipt-capture apps. Snap a photo of a receipt the moment the transaction occurs. Most modern accounting platforms can link directly to your bank account to auto-import transactions, significantly reducing manual entry errors.

6. Neglecting Financial Reports

Many business owners only look at their books when it’s time to file taxes. This is a missed opportunity to understand your business’s health.

-

The Risk: Financial reports—like your Profit & Loss (P&L) and Balance Sheet—are the dashboard of your business. If you aren’t looking at them, you won’t spot shrinking margins, rising operational costs, or unprofitable product lines until it is too late.

-

The Fix: Schedule a “Financial Health Check” meeting with yourself (or your accountant) at the end of every month. Review your key reports to identify trends. Ask yourself: “Where did we spend too much this month?” and “Which income stream is performing best?”

7. Trying to Do Everything Yourself

There comes a point in every growing business where the time spent struggling with complex accounting is worth more than the cost of hiring a professional.

-

The Risk: DIY bookkeeping is a common source of “hidden costs.” You may save a few hundred dollars on an accountant, only to lose thousands in missed tax credits, late fees, or strategic errors born from bad data.

-

The Fix: Determine if your business complexity warrants professional help. Even if you do the daily data entry, having an accountant review your books quarterly can be a massive safeguard against expensive mistakes.

Conclusion: Turning Bookkeeping into a Growth Asset

Bookkeeping should not be a task you fear. When done correctly, it provides the clarity you need to scale, innovate, and sleep better at night. By avoiding these 7 mistakes, you aren’t just protecting yourself from financial loss—you are building a robust foundation that allows you to focus on what you do best: growing your business.

Summary: Critical Bookkeeping Mistakes & Solutions

To help you and your readers quickly identify and address these issues, this table summarizes the most common pitfalls and their actionable solutions.

| Mistake | Potential Consequence | Actionable Solution |

| Mixing Personal & Business Funds | Legal liability (piercing corporate veil) & audit complexity. | Open a dedicated business bank account and credit card. |

| Infrequent Reconciliation | Unnoticed fraudulent charges & bank errors. | Perform a mandatory bank reconciliation every month. |

| Ignoring Cash Flow | Inability to pay bills despite having “profit” on paper. | Regularly monitor your Cash Flow Statement and track A/R. |

| Misclassifying Expenses | Incorrect tax deductions & audit flags. | Maintain a standardized Chart of Accounts for consistency. |

| Delayed Record-Keeping | Missing receipts & loss of accurate data. | Use cloud software with automated receipt-scanning tools. |

| Neglecting Financial Reports | Operating “blind” without trend analysis. | Schedule a monthly “Financial Health Check” to review P&L. |

| DIY Everything | Lost time, costly errors, & missed tax credits. | Hire a professional when complexity exceeds your time/skill. |

Frequently Asked Questions (FAQs): Avoiding Bookkeeping Mistakes in 2026

To help you and your readers further, here are the most common questions regarding small business bookkeeping addressed in the context of 2026 standards.

1. How often should I check my business books?

Answer: At a minimum, you should perform a bank reconciliation once a month. However, with modern cloud-based accounting software that syncs with your bank, it is best practice to review your dashboard weekly. This allows you to catch errors early and maintain an accurate, real-time view of your cash flow.

2. Can I use my personal bank account for my business if I am a freelancer?

Answer: It is highly discouraged, regardless of your business structure. Even if you are a sole proprietor, separating finances creates a clear audit trail. If you ever decide to scale or change your legal structure (to an LLC, for example), having clean, separated records will make the transition significantly easier and prevent legal complications.

3. What is the biggest difference between “Profit” and “Cash Flow”?

Answer: Profit is a measurement of your earnings after expenses are deducted, regardless of when that cash actually hits your bank. Cash Flow measures the timing of the money moving in and out. You can be profitable on paper but still experience a cash flow crisis if your clients take 60 days to pay you while your rent is due today.

4. What should I do if I misclassified an expense months ago?

Answer: Don’t panic, but do address it. If the period is closed (e.g., last year’s taxes are filed), consult with an accountant to see if a reclassification entry is necessary. If the period is still open, simply adjust the transaction in your software. Keeping a note of why the change was made is helpful for your records.

5. Is cloud-based accounting software really necessary in 2026?

Answer: Yes. In 2026, the speed of business requires automation. Cloud software allows for real-time bank feeds, automated receipt scanning, and remote access, which manual spreadsheets cannot match. It significantly reduces human error and ensures that your data is backed up securely.

6. When is the right time to hire a professional accountant?

Answer: If you find that bookkeeping is preventing you from focusing on revenue-generating activities, or if your business has grown to a level of complexity (e.g., managing payroll, inventory, or multi-state tax nexus) that you no longer feel comfortable handling, it is time to hire a professional. Even if you do the daily work yourself, a quarterly review by an accountant is a smart investment.

7. What is the most important financial report I should monitor?

Answer: While the Profit & Loss statement is vital, the Cash Flow Statement is arguably the most critical for small business survival. It tells you exactly how much cash is available to operate your business on a daily basis. Monitoring this regularly helps you avoid the common pitfall of running out of liquid capital.